In this Issue…

A Look Into the Markets

Mortgage Market Guide Candlestick Chart

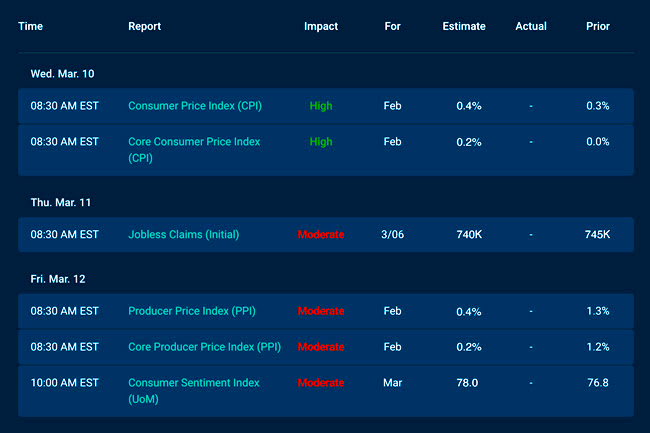

Economic Calendar for the Week of March 8 – March 12

A Look Into the Markets

“It would not be a real problem if inflation shot up to 3%.” … Chicago Fed President Charles Evans 3/3/21

Home loan rates improved modestly week-over-week as the U.S. bond market attempts to stabilize after a sharp increase in rates. Back on Thursday, February 25th, the 10-year yield hit 1.61% and has since declined back beneath 1.50%. This helped mortgage-backed securities (MBS), which drive home loan rates, to also improve in price/rate.

The Sales Pitch Continues

Inflation is the main driver of interest rates. If inflation or inflation expectations move higher, rates move higher, period. The opposite is true. The Fed has had to put on its sales hat recently by continuing to try and sell to the world that inflation in the U.S. will not hit the Fed’s target of 2% over the long-term for three years.

The Fed has noted that inflation will be “volatile.” What does that mean?

Consumer inflation year-over-year is going to rise sharply in the second quarter of 2021. Here’s why. Oil, lumber, and commodity prices like copper, coffee, and grains are up sharply year-over-year. Oil, which is in many consumer products, hovered near $20 a barrel and is now over $60.

“Would need to see inflation exceed 2% in order to even think about starting to get nervous.” Fed President Evans 3/3/21

It would not be surprising to see consumer inflation in the mid to high 2% by May, so Mr. Evans and the entire Fed will have to continue to talk down inflation in order to try and keep rates from increasing further.

“Come on baby, let’s do the Twist” Chubby Checker

The Fed only controls the Fed Funds Rate, an overnight lending rate between banks which impacts short-term loans like credit cards and home equity lines of credit and yes, your savings account at the bank. They do not control long-term rates like mortgages, and proof- positive is the sharp rise in rates in 2021, despite increased bond purchases by the Fed in an effort to stem the rise in rates.

What other tools does the Fed have to try and stabilize long-term rates? The rumor mill is swirling that if rates move higher, the Fed may enforce Operation Twist 3.0. They did it back in 2011, and here’s how it works.

The Fed will sell short-term bonds and purchase long-term bonds. This has the effect of driving down long-term rates while modestly boosting short-term rates. Back in 2011, the impact was significant. The 10-year yield went from a high of 3.75% to a low of 1.44%. However, when the Fed stopped the “Twist” and the manipulation was over, the yield spiked back up to 3% quickly.

Bottom line: Home loan rates remain historically low. Fed bond market manipulation may be required should higher inflation cause another increase in rates. Now is a great time to take advantage of rates before we see an even further rise. If you or someone you know would like to talk about the incredible opportunity that still exists, please contact me.

Looking Ahead

It’s only fitting that next week brings a couple of important reports on inflation. Both the Consumer Price Index and Producer Price Index will be released. The latter tell us what wholesale or producer inflation looks like. If producers have higher costs, those may very well lead to higher consumer costs.

The ongoing $1.9T stimulus negotiations will also be in focus as that giant plan is causing angst in the bond market for its inflationary effects.

Mortgage Market Guide Candlestick Chart

Below is a chart of mortgage-backed securities (MBS). As prices move lower, rates move higher. You can see on the right side of the chart, MBS prices have improved week-over-week, highlighting the modest improvement in rates. There is more room for prices to run higher, thereby helping rates to decline further. The Fed and inflation news will likely be the driver.

Chart: Fannie Mae 30-Year 2% Coupon (Friday, March 5, 2021)

Economic Calendar for the Week of March 8 – 12

The material contained in this newsletter has been prepared by an independent third-party provider. The content is provided for use by real estate, financial services, and other professionals only and is not intended for consumer distribution. The material provided is for informational and educational purposes only and should not be construed as investment and/or mortgage advice. Although the material is deemed to be accurate and reliable, there is no guarantee it is without errors. As your mortgage professional, I am sending you the MMG WEEKLY because I am committed to keeping you updated on the economic events that impact interest rates and how they may affect you. Mortgage Market Guide, LLC is the copyright owner or licensee of the content and/or information in this email, unless otherwise indicated. Mortgage Market Guide, LLC does not grant to you a license to any content, features, or materials in this email. You may not distribute, download, or save a copy of any of the content or screens except as otherwise provided in our Terms and Conditions of Membership, for any purpose.

We are ready to help you find the best possible mortgage solution for your situation. Contact Sheila Siegel at Synergy Financial Group today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}