In this Issue…

A Look Into the Markets

Mortgage Market Guide Candlestick Chart

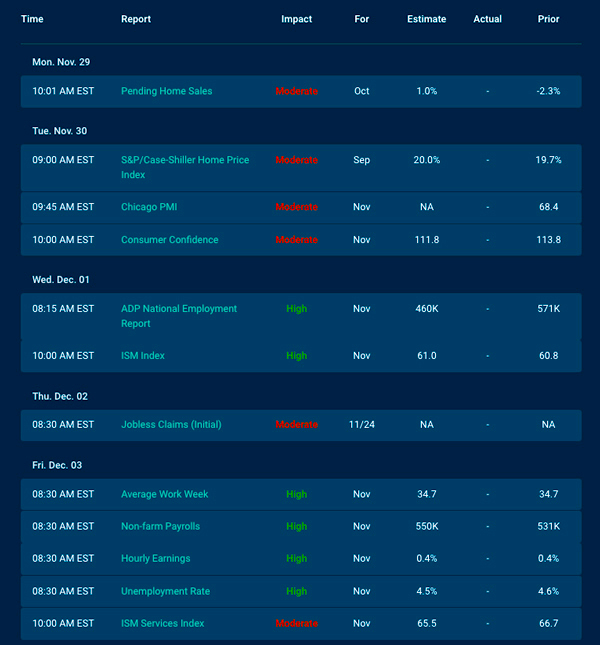

Economic Calendar for the Week of November 29 – December 3

A Look Into the Markets

This past week, we watched mortgage-backed securities (MBSs) make 2021 price lows, which means the highest home loan rates in 2021. Let’s talk about three things moving the markets and what to look for in the week ahead.

1. Consumer Sentiment Remains Near a Decade Low

The Michigan Consumer Sentiment for October was reported at 67.4, hovering near a decade low. The reason? Inflation. Even though we are seeing the highest hourly wage gains in decades, they are being completely outpaced by the rise in prices, which means we are currently seeing negative wage growth, where wages do not keep up with price growth.

This is not a good thing in the longer term. If inflation does not moderate as the Fed had been expecting, this will put pressure on the consumer. If the consumer slows spending due to lack of purchasing power, our Gross Domestic Product (GDP) will decline, as consumer spending makes up two-thirds of our economic growth. We do not want to see consumer spending stall or stop, or we will be seeing bits of stagflation – high inflation and slow growth.

For now, the consumer remains resilient with the ability and willingness to spend. What happens next from a policy response (WH Administration and Federal Reserve) will be very important in 2022. The wrong move at the wrong time could have lingering effects on our economy.

2. MBS Make Fresh 2021 Price Lows

It is important to know that MBSs determine home loan rates, not the 10-yr Note. So even though the 10-yr yield, at 1.67%, has not made a new 2021 high yet, home loan rates hit their highest levels of 2021.

If MBS prices fall much beneath current levels, we are likely to see prices fall further and rates heading higher towards pre-pandemic levels.

This should not be a surprise as the Fed, which we mention above, helped the economy with its pandemic-induced bond-buying program. That bond-buying program is now being tapered and it is scheduled to end in the middle of 2022. Less bond-buying should lead to a gradual increase in home loan rates over time. If you add on the persistently high inflation, one could argue that rates should probably already be higher than present levels.

3. Fed Chair Powell Renominated

President Biden announced he was going to renominate current Fed Chair Jerome Powell to another 4-yr team. He cited his experience and steady hand through the depths of the pandemic. As it relates to housing and mortgage, the Federal Reserve was a savior.

Back in March of 2020, the Fed immediately started a bond-buying program to help stabilize the disrupted MBS market and to pin down long-term mortgage rates. It worked. The Fed’s action created a boom of refinancing and purchase activity which helped grow the economy at a time when many industries were shut down or struggling.

In response to the nomination, the financial markets started pricing in Fed rate hikes as Jerome Powell is less dovish or tolerant of inflation than the other person up for nomination, Lael Brainard.

Stocks were under selling pressure all week in response to the spike in rates, threat of inflation, and increased likelihood of rate hikes.

It remains to be seen when and if the Fed will be able to hike rates sometime in 2022. We have already heard from countries abroad, like the European Union, who recently said they are not likely to hike rates until 2024…citing another wave of Covid and restrictions that will disrupt economic activity.

Bottom line: The Fed is tapering, and inflation is running high, well north of mortgage rates. This is unsustainable over the long term. Either inflation comes down, rates go up, or a bit of both. This means if you are considering a mortgage, take advantage of pandemic-induced rates, while they exist.

Looking Ahead

Next week is Jobs Week. We are going to see the status of the labor market with the ADP report on Wednesday and the Jobs Report on Friday. Remember, the Fed is tasked to promote maximum employment, meaning they want to see maximum employment before hiking rates. How these reports go could have a major impact on rates and the financial markets.

Mortgage Market Guide Candlestick Chart

Mortgage-backed security (MBS) prices are what determine home loan rates. The chart below is the Fannie Mae 30-year 2% coupon, where currently closed loans are being packaged. As prices go higher, rates move lower and vice versa.

The bond made a fresh 2021 intraday low this past week. If MBSs move convincingly beneath the nearby price lows, we are likely to see a further selloff in MBSs, leading to pre-pandemic mortgage rates. BUT, if prices can hold here and at least move sideways, we could see rates stabilize and possibly improve a touch. As you can see this is an important moment in the mortgage world.

Chart: Fannie Mae 30-Year 2% Coupon (Friday, November 26, 2021)

Economic Calendar for the Week of November 29 – December 3

The material contained in this newsletter has been prepared by an independent third-party provider. The content is provided for use by real estate, financial services, and other professionals only and is not intended for consumer distribution. The material provided is for informational and educational purposes only and should not be construed as investment and/or mortgage advice. Although the material is deemed to be accurate and reliable, there is no guarantee it is without errors. As your mortgage professional, I am sending you the MMG WEEKLY because I am committed to keeping you updated on the economic events that impact interest rates and how they may affect you. Mortgage Market Guide, LLC is the copyright owner or licensee of the content and/or information in this email, unless otherwise indicated. Mortgage Market Guide, LLC does not grant to you a license to any content, features, or materials in this email. You may not distribute, download, or save a copy of any of the content or screens except as otherwise provided in our Terms and Conditions of Membership, for any purpose.

We are ready to help you find the best possible mortgage solution for your situation. Contact Sheila Siegel at Synergy Financial Group today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}