In this Issue…

A Look Into the Markets

Mortgage Market Guide Candlestick Chart

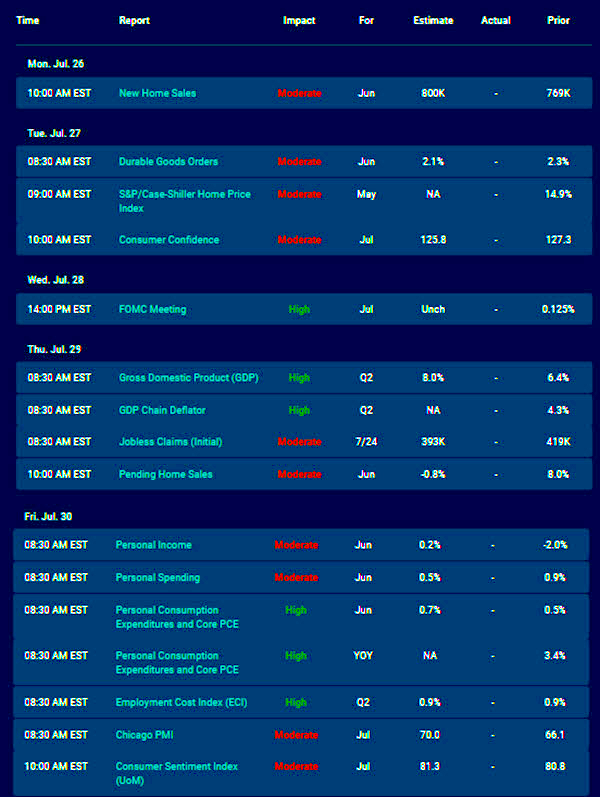

Economic Calendar for the Week of July 26 – July 30

A Look Into the Markets

“Everybody’s Taking the Chance / Safety Dance” – “The Safety Dance” by Men Without Hats

This week long-term rates and home loans rates touched the lowest levels since early February mainly due to rising concerns over the Delta variant of COVID causing more restrictions, shutdowns, and a slowing economy in the future. Let’s talk about what this “safe-haven” trade into the bond market means and what to look for in the days and weeks ahead.

Safe-Haven Trade Explained

During times of high uncertainty around the globe, much like we saw this week with Delta variant fears, we see what is called a “safe-haven” trade. This is where money flows into the safety of the U.S. Dollar and dollar-denominated assets like Treasury and mortgage-backed securities (MBSs), all at the expense of stocks that are deemed risky.

This past Monday, we watched the Dow Jones Industrial Average fall over 700 points, while both Treasury and MBS prices jumped as the safe-haven trade was on.

What Happened?

By midweek long-term rates ticked higher, erasing all the fear. Markets tend to overshoot both to the upside and downside, so by Tuesday, when “cooler heads”prevailed, stocks rallied sharply, erasing all their Monday losses at the expense of bonds and rates.

The reality is that the economy continues to improve, albeit more slowly, but it also means the Fed is not likely to make changes to interest rates or its bond purchase program anytime soon. If rates stay low and the Fed is not changing course, then it’s always a reason for stocks to party and move higher.

On top of the Fed, the Administration is about to embark on another several trillion dollars in spending, intending to boost economic activity.

Now we can only hope and pray the fears surrounding the new Delta variant come to pass. For now, the markets’ fears have been short-lived. We will get a better sense of reality in the weeks ahead as the U.K. just lifted all their COVID restrictions.

Inflation’s Role

For the past couple of months, consumer prices (inflation) have run above 30-year mortgage rates for the first time in 50 years. This is the definition of unsustainable. At some point, either inflation must come down a lot, mortgage rates must rise, or a combination of both.

It’s no wonder the Fed is buying MBSs. Who in their right mind would purchase MBSs when the interest received is not even outpacing inflation?

The Time Is Now

Could rates go lower? Sure. For that to happen, it would likely take something very bad, like a COVID-induced economic stall becoming reality. The markets are not pricing in that scenario right now.

Next, the Fed is under pressure to start tapering their MBS purchases. It may not happen for some time, but when the Fed announces their intention to do so, home loan rates will move higher in a hurry, and today’s rates will be in the rear-view mirror.

Look at the chart section below for yet another reason to take out a new mortgage now.

Bottom Line: For the reasons mentioned, if you or someone you know would like to talk about this incredible interest rate opportunity, please contact me.

Looking Ahead

In the next few weeks, we will be watching to see if COVID causes a problem in the U.K. and even here in the US. If so, we will see more volatility and possibly a revisit of the rates seen this past Monday.

We are also going to see a ton of high-impact economic reports which can move the markets. They include Durable Goods Orders, GDP, and, the Fed’s favorite gauge of inflation, the Core PCE.

And, if that was not enough, next Wednesday the Federal Reserve will issue their Monetary Policy Statement and their thoughts on the economy, interest rates, and tapering their bond purchases.

Mortgage Market Guide Candlestick Chart

Mortgage-backed security (MBS) prices are what determine home loan rates. The chart below is the Fannie Mae 30-Year 2% Coupon, where current closed loans are being packaged.

As prices go higher, rates move lower, and vice versa.

MBSs hit right at their 200-day moving average (purple line), which stopped prices from moving higher still. If prices remain beneath this purple line, home loan rates will remain at or lower than current levels. Should prices be able to break above the purple line, rates could move another leg lower from here.

Chart: Fannie Mae 30-Year 2% Coupon (Friday, July 23, 2021)

Economic Calendar for the Week of July 26 – 30

The material contained in this newsletter has been prepared by an independent third-party provider. The content is provided for use by real estate, financial services, and other professionals only and is not intended for consumer distribution. The material provided is for informational and educational purposes only and should not be construed as investment and/or mortgage advice. Although the material is deemed to be accurate and reliable, there is no guarantee it is without errors. As your mortgage professional, I am sending you the MMG WEEKLY because I am committed to keeping you updated on the economic events that impact interest rates and how they may affect you. Mortgage Market Guide, LLC is the copyright owner or licensee of the content and/or information in this email, unless otherwise indicated. Mortgage Market Guide, LLC does not grant to you a license to any content, features, or materials in this email. You may not distribute, download, or save a copy of any of the content or screens except as otherwise provided in our Terms and Conditions of Membership, for any purpose.

We are ready to help you find the best possible mortgage solution for your situation. Contact Sheila Siegel at Synergy Financial Group today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}